$PFHO Update: I Sold

I’ve been wanting to write a $PFHO update for a while, but life just got the best of me recently. Better late than never.

Short version: I sold out of $PFHO. 51% profit over 13 months.

Here is why I sold, and some words on net-net.

Two reasons

1) Case management has not been grow the way I wanted it to (minor)

My thesis leaned pretty heavily on them growing the case management segment more aggressively as they expand into other states. That was the gem of the business in my mind: high operating leverage, asset-light, sticky relationships, expanding margins. But it just hasn’t happened.

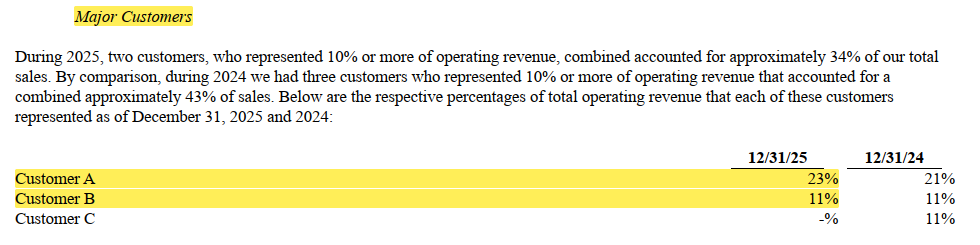

2) Another major customer termination (major)

We already knew this quarter’s revenue would decline from the October 2024 customer termination. Not great, but priced in.

What got me concerned was the 2nd major customer termination in Jan 2026, disclosed in the 10-K released in March 2026. Losing another major customer on top of the first is a much bigger blow. I think this could realistically push PFHO into unprofitability, and that is the net-net thesis breaker for me.

In the same 10-K where they announced the termination, they listed two customers in their concentration disclosure:

If it is B, they could be okay (still not great).

If it is A, it will be pretty ugly.

Let’s actually run the numbers

Here are the 2025 results to anchor on:

Revenue: $6,715,175

Expenses: $5,714,137

EBIT: $1,001,038 (~14.9% margin)

Now, the question is: what happens when you strip out 11% or 23% of revenue? It depends entirely on how fixed the cost base is. PFHO is a tiny company. The staffing is likely lean, you can’t really flex headcount up and down quickly, and most of the cost categories seems fixed:

Salaries & wages: $2.74M (mostly fixed short term)

Professional fees: $931K (semi-fixed; audit, legal, etc.)

Insurance: $333K (semi-fixed)

Outsource service fees: $736K (the one meaningfully variable line)

Data maintenance: $211K (fixed)

G&A: $767K (mostly fixed)

My rough cut: ~80% fixed, ~20% variable. So fixed costs = $4.57M, variable costs = $1.14M.

Running the math with that assumption:

11% loss: Revenue drops to $5.98M, variable costs scale down to ~$1.02M, total expenses become $5.59M → op income of ~$388K (a 61% drop from $1M)

23% loss: Revenue drops to $5.17M, variable costs scale down to ~$880K, total expenses become $5.45M → op income of −$281K (unprofitable from ops)

So losing Customer A (23%) tips them into operating losses. Losing customer B (11%) is survivable but not great. The operating leverage point from the original write-up cuts both ways.

The interest income from the cash pile will provide a cushion; thus PFHO still may post a positive net income. But I want the underlying business to be profitable.

Would I come back?

I think I would be interested in rebuying if

it dips below net cash and the company stays profitable through this

or

it grows its case management segment well

About Net-Net

A quick word on net-nets, since this one was a textbook case.

My average buy was $0.77, sold at an average of $1.17. This gave me 51.4% return over 13 months. Not a home run, but a solid return on a name where the downside was basically capped from day one.

When I bought, $PFHO was the ultimate net-net: cash − total liabilities > market cap, AND the business was good and profitable. You are getting the operating business for free with a discount on the cash. Any improvement in the underlying business would’ve been a bonus.

That bonus never really showed up. Case management didn’t accelerate the way I had hoped, and now they are losing major customers. But because I bought well below net cash with a profitable business underneath, the downside was always limited.

My general playbook on net-nets is:

Hold for at least one year (long-term capital gains treatment)

Sell when it is no longer a net-net, OR

Sell when the business becomes unprofitable

Disclosure: No longer long $PFHO.

Don’t take me seriously. This newsletter is for entertainment and informational purposes only. Nothing here is financial advice. I may hold positions in the stocks discussed, but that doesn’t mean you should. Do your own research, and trust no one blindly, including Scav.